Featured in Tech

Telecom & Internet

Dissecting the main-cream since 15+ years..

DAMAC Properties has launched sales of the world’s first FENDI-styled villas. The 34 properties are located in a private-gated community in the 42 million sq ft AKOYA by DAMAC master development off Umm Suqeim Road in Dubai. Each unit comes with interior designs and decor […]

Builders Infrastructure Real Estate

The forum is free to attend and is a must visit for Architects, Civil Engineers, Contractors, Developers, Distributors, Investors, Government Agencies, State corporation and Structural Engineers.

Builders Infrastructure Manufacturing Real Estate

Lucknow is the capital city of the fourth largest Indian state and is one of the fastest growing cities in India. With burgeoning manufacturing, commercial and retail segments, it has become a preferred real estate destination. Each and every real estate company in Lucknow is […]

Builders Listing Real Estate

Aquaculture, which is the fastest-growing food production process globally, is an emerging trend that is expected to drive the fish and seafood market in the next few years.

Agriculture Food / Beverages Lifestyle People Retail World विश्वगुरु

Sep 7, 2017: There are a huge number of Ashrams in Haridwar, amounting to 300+ and these Ashrams offer accommodation facilities to the huge sea of pilgrims gathering at Haridwar during Kumbh Mela, Ardh Kumbh Mela or other such festive occasions. Stay at any of […]

Art Entertainment Lifestyle People Politics Travel

Cricket may have its politics and complexities but no one can argue with heavy run scoring or wicket taking.

Entertainment Lifestyle Sports World विश्वगुरु

Feb 14, 2016: Public water sports cum amusement parks on must talked banks of river Yumuna can help kids / youngsters from middle and low strata or even Govt schools to strive for Olympics while saving the degrading clean water bodies! Apart from fat cricket […]

Entertainment Lifestyle People Politics Sports

Emotional people’s political and social beliefs are rooted in unprocessed trauma, they never mind supporting any gang of crooks, opportunists, racists and aspiring fascists out of a deep-seated need to see their perceived enemies suffer: tight-wing reactionaries delight only when their enemies have been gleefully trolled via any #messiah namely MuskX, ModiG, MurdochR, MadC, MetaF, MediaP, MaharajaI, MukeshA or anything sounding royal..

Corruption Entertainment Lifestyle Media / PR People Politics Technology World विश्वगुरु

This allows users to search for an activity they would like to partake in and helps them find an available venue, regardless of the time or day – Fitness trainer course fees, best personal trainer certification, gym trainer courses, personal trainer certification online gym trainer course near me, fssa personal trainer course fees, online fitness courses free with certificate, gym trainer course fees in india

Education Entertainment Health Lifestyle People Startup

We are the system, we are the law,

We are corruption, worm in the core,

One of another, laugh ’til you cry,

Faith unto death or a knife in the eye!

Canada-based education company M Square Media (MSM) welcomes a latest major education push, allowing top foreign universities to set up campus shops and award degrees in its bid to enhance the country’s higher education.

Education Entertainment Lifestyle Media / PR People Politics Startup World विश्वगुरु

Biggest security threat comes from inside, not only that it is done deliberately, but it also happens as a result of negligence or profiteering greed of your neighborhood, friends, colleagues and even family. The better the training on data center security, the safer will be overall digital environment for common users..

Infrastructure Law / Legal Linux Software Technology Telecom

More corrupt financial capitalism fostering the culture of scams and collection extortion via suit-boot executives in collusion with cyber cells, call centers and mobile apps mafia. Scams have centered around malpractices in governance: owners and promoters of big companies, political parties and institutions have defrauded citizens to enrich and develop themselves smartly abusing legal, accounting, security, taxation, enforcement, investigative and documentation systems.

Corruption Economy Law / Legal Lifestyle People Politics

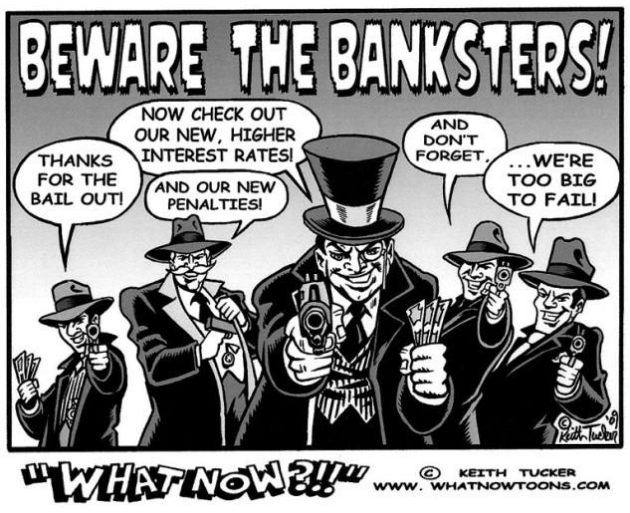

Greatest threat to humanity is the fact that half of the psychopaths are busy in “financing terror” rest are smart sociopaths profiting from “terror in finance”. As guinea pigs, financial revolutions are needed only for 99% commoners, to not fulfill any obligations, to refuse cooperating with the system as it currently exists. Why keep paying our hard-earned rights to the capital mob? We know our resources could be better spent.

Banking / Finance Corruption Economy Infrastructure Law / Legal Lifestyle People Politics Real Estate World विश्वगुरु

AI Buzzwords That Help Fool Investors and Sometimes Workers.. Many of us who understand the importance of quality (not quantity by mindless automation) will continue to enjoy sharp imagery, not derivative ripoffs that are likely plagiarism with presumption of “AInnocence”.

Lifestyle Linux People Software Startup Technology

Aquila AM69 is powered by the TI AM69A Arm-based processor, known for its exceptional performance and reliability

Linux Software Startup Technology

If Ladakh is left open to this kind of free-for-all, with no safeguards, mining contractors and greedy gujju colonizers will surely flock-in to conquer nature.. To be a global leader, Ladakh surely deserves being developed as a crown in Himalayan megalopolis, isn’t bhakt? The tremors of your short-gaming government’s smart actions today will be felt by generations after decades, and justice is extrapolated to be surprisingly denied for all.

Climate Corruption Energy Lifestyle People Politics Travel World विश्वगुरु

But sites and apps are, at best, as fast as they used to ten years ago. In most cases they are even slower, see how clever these greedy AI hyping cronies are, whose leaders are running to abuse great civilizations forever?

Corruption Education Infrastructure Lifestyle Linux Media / PR People Politics Software Startup Technology Telecom World विश्वगुरु

AI helps smart fascists and its strategic partners (लाभार्थी) in storing / staring live data via analytic dashboards to punish anyone instantly for non-conformity or opposing their ideas / diktats to secure Führer’s character anyhow, today’s MODIfied India is a developing case study, while west’s social media brands, global tech giants and fully-bonded political terrorists are co-sponsors!

Economy Lifestyle Media / PR People Politics Software Startup Technology Telecom World विश्वगुरु

Prime helps you create non-AI apps and bots for secure use. With naturally down-to-earth green technologies, tools and easy-to-use interfaces, you can customize personality of your apps, bots, sites and provide instructions for an engaging and personalized experience for your customers and visitors.

Lifestyle Linux Media / PR Software Startup Technology

The real estate sector has been seeing a slump in growth for quite some time now. However, while that is the case with the sector in general, there is at least one segment which seems to be bucking the trend – branded homes in gated societies!

Architecture Builders Infrastructure Investment Law / Legal Lifestyle Listing Real Estate

The one who is here before the start of time and will be there after the end of everything, something beyond time, infinite. It also represents holding infinite energy in Cosmic form.. “एक छोटा, लालच,चोरी, सत्ता, भ्रष्टाचार, घृणा और क्रोध सै पीड़ित अज्ञानी दिमाग एक बड़े शुद्ध और स्वयं गरीब दिमाग की तुलना में कम प्रशंसनीय है।” – विनाशकारी भक्तामर स्तोत्र

Art Lifestyle People Politics World विश्वगुरु

Capitalists vs other ideologies is always Geo-neutral and funny. They plan harming each other for profits of its own gang, and still expect to enjoy flower garlands as return gift birthright now or when the war dust settles..

Banking / Finance Corruption Economy People Politics